-2.png)

With 2017 behind us, it’s time to start thinking about filing your taxes and preparing your farm for the new year. Alex Wilson, a CPA at Yeo & Yeo CPAs & Business Consultants, has offered a few best practices in preparation and planning for 2018. Being aware of the tax reform law changes that impact family farms and agribusinesses is critical, but using a strong financial management software is also a top priority.

Tax Preparation for Agribusiness

Agribusiness accounting is unique—there are many different programs set up, both at federal and state levels, that are there to help with tax breaks for farmers. Your CPA is the person you can trust to connect you with the best opportunities available to you. In agriculture specifically, farmers have an opportunity to maximize returns and minimize tax burdens by utilizing fuel tax credits, the domestic production activities deduction (repealed after the 2017 tax year) and looking at the new Section 199A business deduction that includes pass-throughs from farm co-operatives. A strong Ag CPA will help you benefit from industry-specific rules related to depreciation of Ag equipment and land improvements. Your Ag CPA should understand the in’s and outs of these credits, which are unique to your situation.

Now that the new tax reform bill, Tax Cuts and Job Acts (TCJA), was has officially been signed into law, it will be even more critical for farmers to find a trusted advisor so that they are in-the-know with what changes will be coming their way.

Yeo & Yeo and the MICPA is pleased to jointly offer an eBook, How Will Tax Reform Affect Agribusiness? Visit yeoandyeo.com/tcja-agribusiness to download your free eBook.

Learn more about Yeo & Yeo’s agribusiness services at yeoandyeo.com »

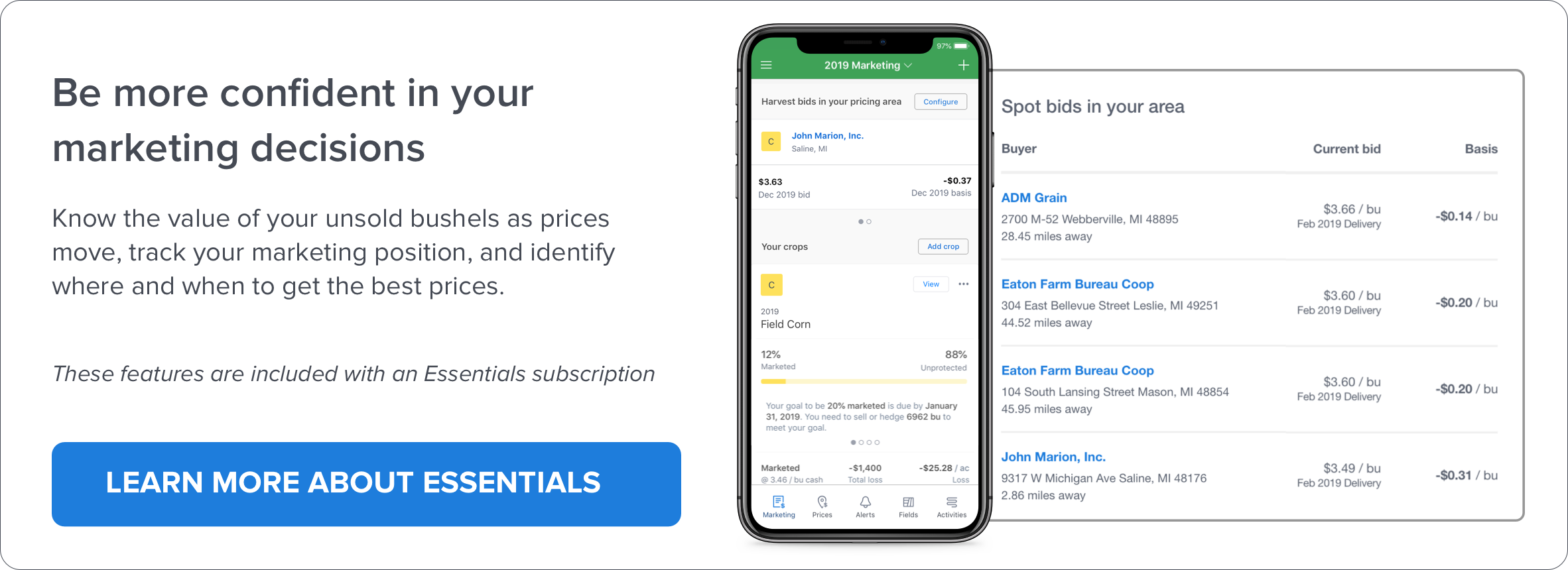

Preparing for 2018

With commodity prices appearing like they're going to be on pace in 2018 with respect to 2017, it is important that you understand where your prices are on a timely basis, so you know where you are likely to end up when the season’s over. There are a few best practice techniques that will help you keep accurate financials:

- Find a strong software system...and use it!

When you are choosing software, you have to consider who will be the one recording the books. In many cases, it doesn't make sense to purchase an expensive software package if you do not have someone tech-savvy dedicated to managing it, because it is likely that you will not be in the position to take advantage of everything the system could do for you. Luckily, there is software out there, such as FarmLogs, that is designed for farmers. These ag software systems give you a better real-time picture than QuickBooks, or excel and green ledger paper.

To get the most value out of your software system, you need to establish regular use. If you only open it once or twice a year, then you will not receive most accurate picture. In addition to regularly using the system, it’s equally imperative to make sure that everything is being recorded properly. The FarmLogs Marketing tool is a great example of software that can help you keep better records and have more insight into your finances. - Have a year-end planning meeting.

Take the time to review the past year and forecast cash flow for the following year. For instance, one way to do this is to map out your future contracts and determine a revenue estimate. These are fairly safe numbers to use, and having this information helps you prepare for the year. These forecasted numbers can aid in making decisions such as deciding if you want to try to pay off any debt, buy new equipment or lease equipment. This can also help you make end of the year purchases, so you know whether or not you should go out and pre-pay for some seed or fertilizer, or wait to pay for your seed in the following January or February and record it as next year's expense. - Your advisor is here to help—keep regular contact throughout the year.

It’s easy to only contact your advisor when taxes are due. In order to maximize the value you receive from your advisor, it’s best not to leave them in the dark all summer. Year-round financial advisement is key to maintaining a strong relationship with your CPA and will help both parties know where each other stands so they can ensure the best decisions are being made for your business or family farm.